Credit Card Choices: FICO Score Guide for 2026

Anúncios

Choosing the right credit card in 2026 hinges on understanding your FICO score, which dictates accessible offers and benefits, ensuring you select a card that aligns with your financial standing and future aspirations.

Anúncios

Navigating the complex landscape of credit card offers can be daunting, but understanding How to Choose the Right Credit Card for Your FICO Score in 2026 is paramount for your financial well-being. This guide will demystify the process, helping you align your credit score with the perfect card to meet your needs and goals.

Anúncios

Understanding your FICO score in 2026

Your FICO score remains a critical indicator of your creditworthiness in 2026, influencing not just credit card approvals but also loan rates and even housing applications. It’s a three-digit number that lenders use to assess the risk of lending money to you. A higher score signifies lower risk, opening doors to better financial products and terms.

The FICO score model continuously evolves, with minor adjustments and updates to incorporate new data points and consumer behavior patterns. While the core components remain consistent, staying informed about these subtle shifts can give you an edge. Understanding what constitutes an excellent, good, fair, or poor score is the first step in strategic credit card selection.

Key factors influencing your FICO score

Several elements contribute to your FICO score, and managing them effectively is crucial for maintaining a healthy credit profile. Payment history stands as the most significant factor, demonstrating your ability to pay debts on time.

- Payment History: Accounts for 35% of your score. Late payments can severely impact your credit.

- Amounts Owed: Makes up 30%. This includes your credit utilization ratio—how much credit you’re using versus your total available credit.

- Length of Credit History: Contributes 15%. Longer histories with responsible use are generally better.

- New Credit: Represents 10%. Too many new credit applications in a short period can be a red flag.

- Credit Mix: Accounts for 10%. A healthy mix of different credit types (e.g., credit cards, installment loans) can be beneficial.

Regularly monitoring your credit report from all three major bureaus (Equifax, Experian, and TransUnion) is essential. This allows you to identify any discrepancies or fraudulent activity that could negatively affect your score, ensuring accuracy and protecting your financial standing.

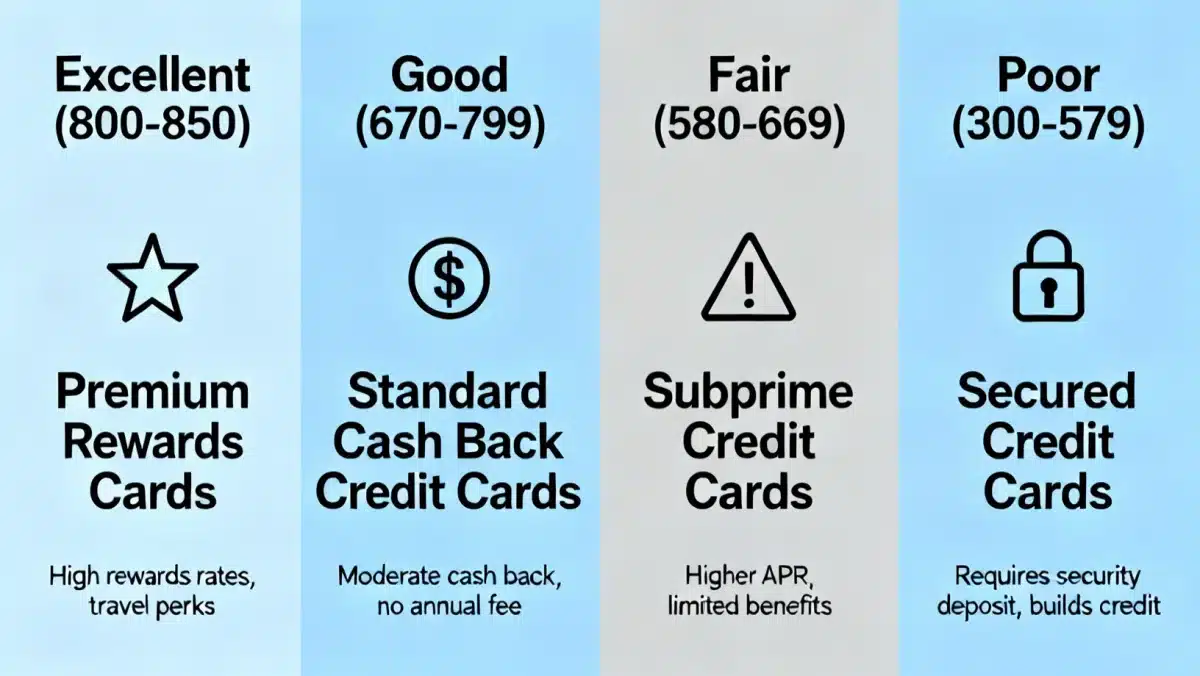

Credit cards for excellent FICO scores (780+)

For individuals with excellent FICO scores (typically 780 and above), the world of credit cards offers a plethora of premium options designed to reward responsible financial behavior. These cards often come with lucrative sign-up bonuses, high reward rates, and exclusive perks that can significantly enhance your spending power and lifestyle.

Lenders view those with excellent scores as low-risk, making them eligible for the most competitive interest rates and the highest credit limits. This financial freedom allows you to choose cards that truly align with your spending habits and financial goals, whether that’s maximizing travel rewards or earning substantial cash back on everyday purchases.

Premium rewards and benefits

Cards tailored for excellent credit often feature generous reward programs. These can include accelerated points on specific spending categories, travel credits, airport lounge access, and comprehensive travel insurance. Some offer concierge services or exclusive event access, adding significant value beyond just financial rewards.

- Travel Rewards Cards: Ideal for frequent travelers, offering miles or points convertible to flights, hotels, and travel experiences.

- Cash Back Cards: Provide a percentage of your spending back as cash, often with tiered rewards for different categories.

- Luxury Perks: Access to airport lounges, travel insurance, concierge services, and exclusive experiences.

When selecting a premium card, it’s crucial to evaluate the annual fees against the benefits offered. While some high-end cards carry substantial annual fees, the value of their rewards and perks can often outweigh these costs for the right user. Always read the fine print and understand the redemption options to ensure the card truly serves your interests.

Optimizing choices for good FICO scores (670-739)

A good FICO score (generally between 670 and 739) places you in a strong position to access a wide range of credit card products. While you might not qualify for the absolute top-tier luxury cards, you’ll still find excellent options that offer competitive rewards, reasonable interest rates, and opportunities to further improve your credit health.

The focus here should be on cards that provide solid benefits without exorbitant annual fees, and those that can help transition your score from ‘good’ to ‘excellent.’ This often means looking for cards with decent cash back rates, introductory 0% APR offers, and manageable credit limits that you can responsibly utilize.

Building on a solid foundation

For those with good credit, securing a card with a low interest rate is often a priority, especially if you anticipate carrying a balance occasionally. Additionally, cards that offer a sign-up bonus after meeting a certain spending threshold can provide a valuable boost without requiring an excellent score.

- Low-Interest Rate Cards: Beneficial if you sometimes carry a balance, minimizing interest charges.

- Cash Back Rewards: Many cards offer 1% to 2% cash back on all purchases or higher rates in specific categories.

- Balance Transfer Offers: Can help consolidate debt from higher-interest cards, often with an introductory 0% APR.

It’s important to continue practicing good credit habits, such as paying on time and keeping your credit utilization low. By doing so, you can steadily improve your FICO score, eventually unlocking access to even more exclusive card offers and better financial terms in the future.

Navigating credit cards with fair FICO scores (580-669)

If your FICO score falls into the fair range (580-669), your credit card options become a bit more limited, but certainly not non-existent. This score range indicates that while you may have had some credit challenges in the past, you are likely on the path to improving your financial standing. The key here is to choose cards designed to help build or rebuild credit responsibly.

Avoid applying for cards that are clearly out of your league, as multiple rejections can further negatively impact your score. Instead, focus on cards specifically marketed towards those with fair credit, as these lenders are more likely to approve your application and provide a stepping stone to better credit.

Secured cards and credit builder options

Secured credit cards are often the best choice for individuals with fair credit. These cards require a cash deposit, which typically becomes your credit limit. This deposit acts as collateral, reducing the risk for the lender and making it easier for you to get approved.

The beauty of a secured card is that it reports your payment activity to credit bureaus, just like a traditional unsecured card. By making timely payments and keeping your utilization low, you can demonstrate responsible credit behavior and gradually improve your FICO score. Many secured cards even offer a path to upgrade to an unsecured card after a period of good behavior.

- Secured Credit Cards: Require a deposit, which often becomes your credit limit, ideal for building credit.

- Credit Builder Loans: While not credit cards, these loans help establish payment history without needing collateral upfront.

- Cards for Fair Credit: Some unsecured cards are available, often with higher interest rates and lower limits, but still valuable for building credit.

Another option to consider is becoming an authorized user on someone else’s credit card, provided that person has excellent credit and responsible spending habits. This can allow their positive payment history to reflect on your credit report, offering a boost without taking on new debt yourself. However, ensure the primary cardholder is trustworthy, as their mismanagement could also affect your score.

Strategies for very poor FICO scores (below 580)

Having a very poor FICO score (below 580) can feel discouraging, but it’s not a permanent state. This score range often results from significant credit challenges like bankruptcies, foreclosures, or a history of missed payments. While traditional credit cards may be out of reach, there are still actionable steps you can take to start rebuilding your credit in 2026.

The primary goal here is to establish a positive payment history and demonstrate financial responsibility. This foundation will be crucial for gradually improving your score and eventually qualifying for better credit products. Patience and discipline are key during this rebuilding phase.

Rebuilding your credit foundation

For those with very poor credit, secured credit cards are often the most accessible and effective tool. As mentioned, they require a deposit, but this provides a safe way to show lenders you can manage credit responsibly. Look for secured cards with low annual fees and those that report to all three major credit bureaus.

- Secured Credit Cards: Your best bet to start building positive payment history.

- Credit Builder Loans: Specifically designed to help establish credit by saving money and making regular payments.

- Authorized User Status: If a trusted individual with good credit can add you, it might help, but proceed with caution.

Beyond specific credit products, focus on fundamental financial habits. Pay all your bills on time, even those not typically reported to credit bureaus (like rent or utilities), as some services now offer reporting options. Create a budget, stick to it, and work on reducing any existing debt. These actions, combined with responsible use of secured products, will pave the way for a healthier financial future.

Understanding credit card terms and fees in 2026

Choosing the right credit card isn’t just about your FICO score; it’s also about meticulously understanding the terms and fees associated with each card. In 2026, credit card companies continue to offer a diverse array of products, each with its own specific conditions. Overlooking these details can lead to unexpected costs and diminish the value of any rewards or benefits.

It’s crucial to read the cardholder agreement thoroughly before committing. Pay close attention to interest rates, annual fees, late payment penalties, and foreign transaction fees, especially if you plan to travel internationally. A card that seems appealing due to its rewards might turn out to be costly if its fees are not managed effectively.

Key terms and fees to evaluate

The annual percentage rate (APR) is one of the most important factors, particularly if you anticipate carrying a balance. A high APR can quickly erode any cash back or points you earn. Some cards offer introductory 0% APR periods, which can be beneficial for large purchases or balance transfers, but be mindful of when these periods end and the standard APR kicks in.

- Annual Percentage Rate (APR): The interest rate charged on unpaid balances. Look for competitive rates or 0% introductory offers.

- Annual Fee: A yearly charge for having the card. Evaluate if the benefits outweigh this cost.

- Late Payment Fees: Penalties for missing payment due dates. Always pay on time to avoid these.

- Foreign Transaction Fees: A percentage charged on purchases made outside the U.S. or in foreign currency.

- Cash Advance Fees: Charges for withdrawing cash using your credit card, often with high APRs.

Furthermore, be aware of balance transfer fees if you’re consolidating debt, and penalty APRs that can be triggered by late payments. Understanding these terms ensures you can use your credit card wisely, avoiding unnecessary charges and maximizing its financial utility. A well-informed decision about terms and fees is as important as matching the card to your FICO score.

Maximizing credit card rewards and benefits

Once you’ve chosen a credit card that aligns with your FICO score and financial situation, the next step is to strategically maximize its rewards and benefits. Credit cards offer a diverse range of incentives, from cash back and travel points to exclusive discounts and insurance protections. Understanding how to leverage these effectively can significantly enhance your financial life in 2026.

The key to maximizing rewards lies in aligning your spending habits with the card’s reward structure. If your card offers bonus points on groceries, make sure to use it for all your supermarket purchases. Similarly, if it provides travel credits, plan your vacations around those benefits to get the most value.

Strategic spending for optimal returns

Many rewards cards come with rotating bonus categories or offer accelerated earnings on specific types of purchases. Keeping track of these categories and adapting your spending can lead to substantial gains. Combining different cards, each optimized for different spending categories, is a common strategy for high-earning individuals.

- Align Spending with Bonus Categories: Use cards that offer higher rewards for your most frequent spending.

- Utilize Sign-Up Bonuses: Meet spending requirements for new cards to earn substantial initial rewards.

- Redeem Rewards Wisely: Understand the value of your points/miles and choose redemption options that offer the best return.

- Take Advantage of Perks: Don’t overlook benefits like purchase protection, extended warranties, or rental car insurance.

Beyond direct rewards, many credit cards offer a suite of additional benefits that can save you money or provide peace of mind. These can include travel insurance, extended warranties on purchases, car rental insurance, and fraud protection. Familiarize yourself with all the features your card offers and integrate them into your financial planning to ensure you’re getting the maximum value out of your chosen credit card.

| Key Point | Brief Description |

|---|---|

| FICO Score Importance | Your FICO score dictates credit card eligibility and terms, making it crucial for informed choices. |

| Score-Specific Cards | Different FICO ranges (excellent, good, fair, poor) align with specific card types, from premium to secured. |

| Terms & Fees | Always review APR, annual fees, and other charges to avoid unexpected costs and maximize value. |

| Maximize Rewards | Align spending with card benefits and redeem rewards strategically for optimal financial returns. |

Frequently asked questions about FICO scores and credit cards

In 2026, a FICO score of 670 to 739 is generally considered ‘good,’ while 740 to 799 is ‘very good,’ and 800+ is ‘exceptional.’ Lenders use these ranges to assess your creditworthiness, with higher scores leading to better credit card offers and loan terms.

To improve your FICO score, focus on paying all bills on time, keeping credit utilization below 30%, avoiding new credit applications too frequently, and maintaining a diverse credit mix. Consistent responsible behavior over time is key to seeing significant improvement.

Yes, secured credit cards are an excellent option for individuals with low FICO scores. They require a security deposit, which acts as collateral, making them easier to obtain. Responsible use, including on-time payments, helps build positive credit history and improve your score over time.

Always check the Annual Percentage Rate (APR), any annual fees, late payment fees, and foreign transaction fees. Understanding these terms is crucial to avoid unexpected costs and ensure the card aligns with your financial habits and intended use.

Credit card rewards offer points, miles, or cash back based on your spending. Maximize them by understanding your card’s bonus categories, utilizing sign-up bonuses, and redeeming rewards strategically for the highest value, often by aligning them with your regular expenses.

Conclusion

Choosing the right credit card in 2026 is a strategic financial decision deeply intertwined with your FICO score. By understanding where your score stands, you can effectively navigate the myriad of options available, from premium rewards cards for excellent credit to secured cards designed for rebuilding. Remember to meticulously evaluate terms, fees, and benefits to ensure the card not only aligns with your current financial health but also supports your future credit-building goals. Responsible credit management, combined with informed choices, will empower you to leverage your credit card as a powerful tool for financial success.