Emergency Fund Creation: Save 6 Months by Dec 2026

Anúncios

Achieving an emergency fund that covers six months of living expenses by December 2026 is an attainable goal through strategic financial planning, diligent saving, and disciplined expense management.

Anúncios

Embarking on the journey of emergency fund creation is one of the most crucial steps towards financial stability. This guide will walk you through the practical steps to accumulate six months’ worth of living expenses by December 2026, offering actionable strategies to make this significant financial goal a reality.

Anúncios

Understanding the ‘Why’ Behind an Emergency Fund

Before diving into the ‘how,’ it is vital to grasp the fundamental importance of an emergency fund. This financial safety net is not merely a suggestion but a critical component of personal financial health, designed to protect you from life’s inevitable curveballs.

An emergency fund acts as a buffer, preventing you from falling into debt when unexpected expenses arise. Think of it as your personal financial shield against job loss, medical emergencies, car repairs, or unforeseen home maintenance costs. Without it, these events often lead to high-interest credit card debt or dipping into long-term investments, derailing your financial progress.

The Psychological Benefits of Financial Security

Beyond the practical advantages, having a robust emergency fund provides immense psychological peace of mind. Knowing you have a financial cushion reduces stress and anxiety, allowing you to make clear-headed decisions during challenging times rather than reacting out of panic.

- Reduced Stress: Financial worries are a leading cause of stress; an emergency fund mitigates this significantly.

- Better Decision-Making: You can take time to find a new job or evaluate options without immediate financial pressure.

- Protection of Investments: Avoid liquidating long-term investments prematurely during market downturns.

- Increased Confidence: A sense of control over your financial future empowers you to pursue other goals.

Understanding these benefits reinforces the commitment needed for emergency fund creation, transforming it from a chore into an empowering financial endeavor. It’s about building resilience and preparing for an uncertain future.

Calculating Your Target: Six Months of Living Expenses

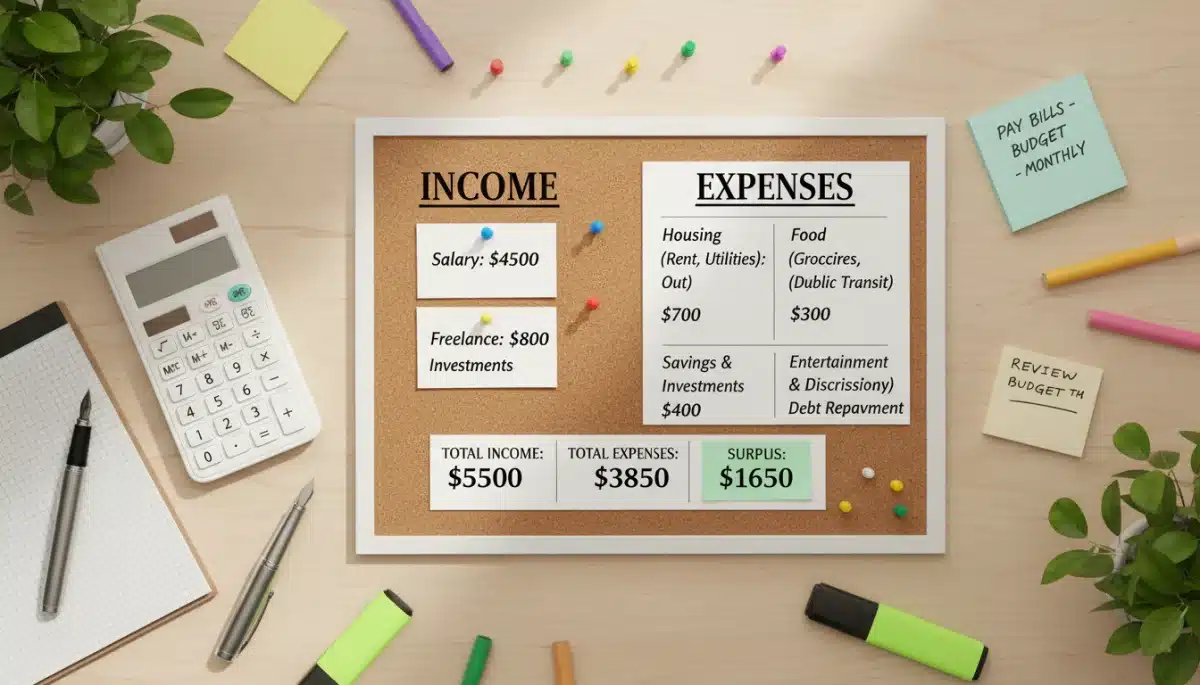

The first concrete step in your emergency fund creation journey is to accurately determine your target amount. Six months of living expenses isn’t a random figure; it’s a widely recommended benchmark that provides substantial coverage for most unforeseen circumstances.

Start by meticulously tracking your monthly expenditures. This isn’t just about big bills; it includes every dollar spent. Many people underestimate their true living costs, so a detailed review is essential for an accurate calculation. Consider all your essential outgoings, not just discretionary spending.

Essential vs. Discretionary Spending

When calculating your living expenses, distinguish between essential and discretionary spending. Your emergency fund should primarily cover essentials, though a small buffer for minimal discretionary spending can be included for comfort during an emergency.

- Essential Expenses: Housing (rent/mortgage), utilities, groceries, transportation, insurance premiums, debt minimums, basic healthcare.

- Discretionary Expenses: Dining out, entertainment, subscriptions (non-essential), vacations, luxury purchases.

Once you have a clear picture of your average monthly essential expenses, multiply that figure by six. This will be your emergency fund target. For example, if your essential monthly expenses are $3,000, your target fund should be $18,000. This clear, quantifiable goal is crucial for effective planning and motivation.

Strategic Budgeting: Finding Funds to Save

With your target amount established, the next phase of emergency fund creation involves strategic budgeting to identify where you can free up cash for saving. This isn’t about deprivation, but about intentional spending and making choices that align with your financial goals.

Begin by creating a detailed budget if you don’t already have one. There are numerous budgeting methods available, from the 50/30/20 rule to zero-based budgeting, each offering a structured approach to managing your income and expenses. The key is to find a method that works for you and stick to it consistently.

Identifying Areas for Reduction

Review your current spending habits with a critical eye. Look for areas where you can realistically cut back without significantly impacting your quality of life. Even small, consistent reductions can add up over time.

- Subscription Services: Cancel unused streaming platforms, gym memberships, or app subscriptions.

- Eating Out: Cook more meals at home and pack lunches for work.

- Transportation: Consider carpooling, public transport, or walking/biking for shorter distances.

- Impulse Purchases: Implement a “24-hour rule” before buying non-essential items.

The goal is to reallocate funds from discretionary spending towards your emergency fund. This process requires discipline and a clear understanding of your priorities. Remember, these adjustments are temporary sacrifices for long-term financial security.

Boosting Your Income: Accelerating Your Savings

While cutting expenses is vital, increasing your income can significantly accelerate your emergency fund creation. This approach allows you to contribute more to your savings without feeling overly restricted in your daily spending.

Explore various avenues for earning additional money. This could range from leveraging existing skills to taking on new opportunities. The gig economy offers a plethora of options for supplemental income, often with flexible schedules.

Side Hustles and Additional Income Streams

Consider what unique skills or resources you possess that could generate extra cash. Even a few hundred dollars extra each month can make a substantial difference in reaching your goal by December 2026.

- Freelancing: Offer services like writing, graphic design, web development, or social media management.

- Online Surveys/Tasks: Participate in paid surveys or micro-task platforms in your spare time.

- Selling Unused Items: Declutter your home and sell clothes, electronics, or furniture you no longer need.

- Part-Time Work: Take on a part-time job or temporary assignments.

Every additional dollar earned and directed towards your emergency fund brings you closer to your target. This proactive approach not only builds your savings faster but can also enhance your skills and provide valuable experience.

Automating Your Savings and Tracking Progress

Consistency is paramount in emergency fund creation. One of the most effective strategies to ensure consistent contributions is to automate your savings. This removes the temptation to spend the money and makes saving a non-negotiable part of your financial routine.

Set up an automatic transfer from your checking account to a separate savings account specifically designated for your emergency fund. Schedule this transfer to occur on your payday, so you ‘pay yourself first’ before other expenses arise. Even if it’s a small amount initially, consistent automation will build momentum.

Monitoring Your Emergency Fund Growth

Regularly track your progress towards your December 2026 goal. Seeing your fund grow provides motivation and reinforces positive financial habits. Use a spreadsheet, a budgeting app, or even a simple chart to visualize your savings journey.

- Dedicated Savings Account: Keep your emergency fund in a separate, easily accessible, but distinct high-yield savings account.

- Regular Reviews: Check your progress monthly or bi-monthly to ensure you’re on track.

- Adjust as Needed: If your income or expenses change, adjust your automated savings amount accordingly.

- Celebrate Milestones: Acknowledge your achievements, like reaching your first month’s expenses, to stay motivated.

Automating your savings ensures steady growth, and consistent tracking keeps you engaged and accountable. These practices transform the abstract goal of an emergency fund into a tangible, achievable reality.

Maintaining Discipline and Avoiding Pitfalls

Even with a clear plan, the journey of emergency fund creation can present challenges. Maintaining discipline is crucial, especially when faced with temptations or unexpected financial pressures. Remember your ‘why’ and stay focused on the long-term benefit of financial security.

One common pitfall is dipping into the emergency fund for non-emergencies. It’s vital to define what constitutes a true emergency for you and stick to that definition. The fund is for genuine crises, not for impulse purchases or vacations.

Common Obstacles and How to Overcome Them

Anticipating potential hurdles can help you develop strategies to navigate them effectively, ensuring your emergency fund remains intact and continues to grow.

- Lifestyle Inflation: As income increases, resist the urge to immediately upgrade your lifestyle; instead, increase your savings rate.

- Debt vs. Savings Dilemma: While paying high-interest debt is important, a small emergency fund (e.g., $1,000) should be prioritized first to prevent new debt.

- Lack of Motivation: Revisit your goals, visualize the security your fund provides, and remind yourself of the December 2026 deadline.

- Unexpected Expenses (non-emergency): Plan for predictable irregular expenses (e.g., holiday gifts, annual car registration) in a separate sinking fund rather than your emergency fund.

By understanding these potential pitfalls and actively working to avoid them, you strengthen your resolve and ensure your emergency fund creation stays on track towards its December 2026 completion.

The Finish Line: What Happens After December 2026?

Reaching your goal of six months’ living expenses by December 2026 is a monumental achievement. It signifies a significant milestone in your financial journey and establishes a strong foundation for future wealth building. But what comes next?

Once your emergency fund is fully funded, the money should remain untouched, serving its purpose as a safety net. Your financial focus can then shift towards other important goals, such as investing for retirement, saving for a down payment on a home, or funding your children’s education.

Beyond the Emergency Fund

Your disciplined approach to emergency fund creation has likely instilled valuable financial habits that you can now apply to other areas of your life. This new financial literacy and self-control are assets that will serve you well for years to come.

- Investment Opportunities: Explore diversified investment portfolios to grow your wealth.

- Debt Repayment Acceleration: Pay down any remaining high-interest debt aggressively.

- Long-Term Savings: Contribute regularly to retirement accounts like 401(k)s and IRAs.

- Financial Independence: Continue to learn and adapt your financial strategies to work towards broader financial freedom.

December 2026 is not just an endpoint; it’s a launchpad. The discipline and planning used to build your emergency fund will be the same qualities that propel you towards achieving even greater financial aspirations.

| Key Strategy | Brief Description |

|---|---|

| Calculate Target | Determine your monthly essential expenses and multiply by six for your savings goal. |

| Strategic Budgeting | Identify and reduce discretionary spending to free up funds for saving. |

| Automate Savings | Set up regular, automatic transfers to a dedicated emergency fund account. |

| Boost Income | Explore side hustles or additional income streams to accelerate fund growth. |

Frequently Asked Questions About Emergency Funds

Six months provides a robust safety net, offering sufficient time to recover from major financial disruptions like job loss or significant medical events. It balances comprehensive coverage with an achievable savings goal, giving ample breathing room.

It’s best kept in a separate, easily accessible, high-yield savings account. This ensures liquidity while earning a modest return, keeping it distinct from your everyday spending money and less tempting to use for non-emergencies.

No, an emergency fund should strictly be reserved for true emergencies like job loss, unexpected medical bills, or major home/car repairs. Using it for vacations or impulse buys defeats its purpose and leaves you vulnerable.

A common strategy is to first save a small starter emergency fund (e.g., $1,000) to prevent new debt. Then, focus aggressively on paying off high-interest debt, and once that’s managed, return to fully funding your emergency savings.

Set clear, measurable goals, track your progress regularly, and celebrate small milestones. Remind yourself of the security and peace of mind the fund provides, and visualize reaching your December 2026 target.

Conclusion

Achieving your goal of an emergency fund covering six months of living expenses by December 2026 is an ambitious yet entirely attainable feat. It requires a combination of diligent planning, disciplined saving, and a commitment to your financial well-being. By understanding the importance of this safety net, meticulously calculating your target, strategically budgeting, exploring income-boosting opportunities, and consistently tracking your progress, you are not just saving money; you are building a resilient financial future. The journey of emergency fund creation is transformative, equipping you with the habits and confidence to navigate life’s uncertainties and pursue greater financial aspirations beyond 2026.