Paycheck Breakdown 2026: Deductions, Net Pay, and Financial Education

Anúncios

Understanding your 2026 paycheck is crucial for financial well-being, as it involves deciphering gross pay, mandatory and voluntary deductions, and ultimately, your net pay, which impacts budgeting and savings.

Anúncios

Have you ever looked at your paycheck and wondered where all the money goes? In 2026, navigating your earnings can feel complex, but mastering the art of understanding your paycheck in 2026: a financial education breakdown of deductions and net pay is a fundamental step towards financial empowerment. This guide will demystify the numbers, helping you grasp exactly how your gross income transforms into the net amount you take home.

Anúncios

Decoding Gross Pay: The Starting Point of Your Earnings

Gross pay represents the total amount of money you earn before any deductions are taken out. It’s the headline figure your employer quotes, but it’s rarely the amount that hits your bank account. Understanding this initial figure is vital because it forms the basis for all subsequent calculations and deductions, both mandatory and voluntary.

For most employees, gross pay is calculated based on an hourly wage multiplied by the hours worked, or a fixed annual salary divided by the number of pay periods. Overtime hours, bonuses, and commissions also contribute to your gross income, increasing your overall earnings before taxes and other withholdings. It’s important to keep track of these components as they can significantly influence your financial planning for the year.

Hourly vs. Salaried Income

Whether you’re paid hourly or on a salary, your gross pay calculation differs. Hourly employees often see fluctuations based on hours worked, while salaried individuals typically receive a consistent amount each pay period. Both, however, are subject to the same types of deductions.

- Hourly Wages: Total hours worked multiplied by the hourly rate, plus any overtime.

- Salaried Income: Annual salary divided by the number of pay periods (e.g., 26 for bi-weekly, 12 for monthly).

- Additional Earnings: Bonuses, commissions, and tips are added to your base gross pay.

Knowing your gross pay is the first step in understanding your financial picture. It’s the maximum you could possibly earn in a given period, and every dollar deducted from it serves a specific purpose, whether it’s for taxes, benefits, or retirement savings. This initial figure sets the stage for a comprehensive financial education.

Mandatory Deductions: What the Government Requires

Mandatory deductions are non-negotiable withholdings from your gross pay, primarily imposed by federal, state, and local governments. These deductions fund essential public services and social programs, and understanding them is crucial for any American worker. These are not optional, and their amounts are determined by law and your individual financial situation, such as your filing status and number of allowances.

The primary mandatory deductions include federal income tax, state income tax (in most states), and Federal Insurance Contributions Act (FICA) taxes, which cover Social Security and Medicare. Each of these plays a significant role in reducing your take-home pay, but also contributes to your future financial security and the welfare of society.

Federal Income Tax

Federal income tax is levied by the U.S. government on your earnings. The amount withheld depends on your income level, filing status (single, married filing jointly, etc.), and the information you provide on your W-4 form. It’s a progressive tax, meaning higher earners pay a larger percentage of their income in taxes.

- Tax Brackets: Income is taxed at different rates based on specified ranges.

- W-4 Form: Determines how much tax is withheld from each paycheck based on your elections.

- Adjustments: Can be adjusted throughout the year to avoid under- or over-withholding.

State and Local Income Taxes

Many states and some localities also impose their own income taxes. These vary widely across the country, with some states having no income tax at all, while others have progressive or flat tax rates. It’s important to be aware of your specific state and local tax obligations, as they can significantly impact your net pay.

FICA taxes are another critical mandatory deduction. This includes Social Security, which provides benefits for retirees, the disabled, and survivors, and Medicare, which funds healthcare for individuals aged 65 or older and those with certain disabilities. These taxes are a fixed percentage of your earnings, up to a certain income limit for Social Security.

Voluntary Deductions: Investing in Your Future and Well-being

Beyond the mandatory deductions, your paycheck often includes voluntary withholdings. These are amounts you choose to have deducted from your pay, typically for benefits or savings plans offered by your employer. While optional, these deductions are often highly beneficial, contributing to your health, financial security, and long-term goals.

Common voluntary deductions include contributions to health insurance, dental and vision plans, retirement accounts like 401(k)s, and flexible spending accounts (FSAs) or health savings accounts (HSAs). Making informed choices about these deductions is a cornerstone of effective financial planning and can lead to significant savings and benefits down the line.

Health Insurance Premiums

Most employers offer health insurance plans, and your share of the premium is deducted from your paycheck. This ensures you have access to medical care, which is a critical aspect of personal well-being and financial stability, preventing potentially catastrophic medical bills.

Retirement contributions, such as those to a 401(k) or 403(b), are another common voluntary deduction. These plans allow you to save for retirement on a tax-advantaged basis, often with an employer match, which is essentially free money towards your future. Contributing to these accounts early and consistently can significantly boost your retirement nest egg.

Other Voluntary Benefits

- Dental and Vision Insurance: Often offered separately from health insurance to cover specific care.

- Life and Disability Insurance: Provides financial protection for you and your family in unforeseen circumstances.

- Flexible Spending Accounts (FSAs) / Health Savings Accounts (HSAs): Allow you to set aside pre-tax money for healthcare or dependent care expenses.

- Union Dues: If you are part of a union, dues are typically deducted from your pay.

- Loan Repayments: Some employers offer options to repay company loans or advances directly from your paycheck.

Carefully evaluating your options for voluntary deductions is a smart financial move. These benefits can provide peace of mind, save you money on taxes, and help you build a secure future. It’s important to review your choices annually during open enrollment periods to ensure they still align with your needs.

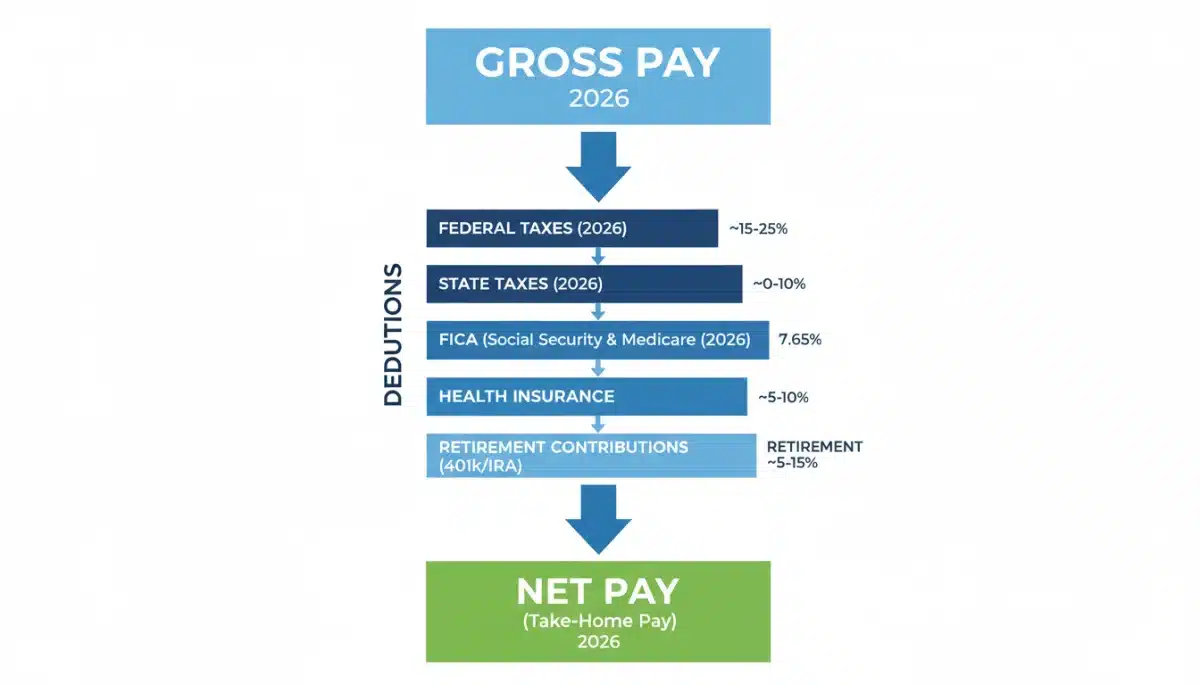

Calculating Net Pay: What You Actually Take Home

Net pay, often referred to as your take-home pay, is the amount of money you receive after all mandatory and voluntary deductions have been subtracted from your gross pay. This is the figure that truly matters for your day-to-day budgeting, savings, and spending. Understanding how it’s calculated allows you to accurately plan your finances and avoid any surprises.

The journey from gross to net pay involves a series of subtractions, and each deduction reduces the final amount. While some deductions are fixed, others, like income tax withholding, can be influenced by your W-4 elections. Therefore, a clear understanding of your net pay calculation is fundamental to managing your personal finances effectively.

The Net Pay Formula

The basic formula for net pay is straightforward: Gross Pay – Total Deductions = Net Pay. However, the complexity lies in accurately identifying and calculating each deduction. It’s not just about subtracting a lump sum; it’s about understanding the individual components that contribute to that total reduction.

- Gross Pay: Your total earnings before any deductions.

- Mandatory Deductions: Federal income tax, state income tax, FICA (Social Security and Medicare).

- Voluntary Deductions: Health insurance, retirement contributions, other benefits.

Each deduction type is calculated based on specific rules and rates. For example, federal income tax is based on your taxable income, which might be lower than your gross income if you have pre-tax deductions like 401(k) contributions or health insurance premiums. This pre-tax treatment can effectively lower your overall tax burden.

Knowing your net pay is essential for creating a realistic budget. It tells you exactly how much money you have available for living expenses, debt repayment, and discretionary spending. Regularly reviewing your pay stubs can help you verify the accuracy of these calculations and identify any discrepancies.

Impact of Tax Law Changes in 2026 on Your Paycheck

Tax laws are not static, and changes can significantly affect your paycheck from year to year. As we look towards 2026, it’s prudent to consider how potential legislative adjustments might impact your gross and net pay. Staying informed about these changes is crucial for proactive financial planning and ensuring you optimize your tax situation.

Governments often adjust tax brackets, deduction limits, and credit availability. These modifications can alter the amount of federal and state income tax withheld, directly influencing your take-home pay. Understanding these potential shifts allows you to adjust your W-4 elections or financial strategies accordingly, preventing unexpected tax liabilities or refunds.

Anticipated Federal Tax Adjustments

While specific changes for 2026 are subject to legislative processes, historical patterns suggest adjustments to federal income tax brackets due to inflation, and potentially changes to standard deductions and personal exemptions. These adjustments are designed to keep the tax system equitable but require taxpayers to remain vigilant.

- Inflation Adjustments: Tax brackets and standard deductions are often indexed for inflation.

- Policy Shifts: New administrations or legislative priorities can introduce significant tax reforms.

- Credit Changes: Eligibility and amounts for tax credits (e.g., child tax credit) may be altered.

State tax laws also evolve, with some states re-evaluating their income tax rates, property taxes, or sales taxes. These changes, though sometimes less direct than federal income tax, can still impact your overall financial burden and, by extension, your perception of your net pay.

It is advisable to consult reliable financial news sources, government tax agency websites, or a tax professional as 2026 approaches to get the most accurate and up-to-date information regarding tax law changes. Proactive awareness allows you to make timely adjustments to your payroll withholdings and financial plans.

Strategies for Optimizing Your Net Pay and Financial Health

Maximizing your net pay isn’t always about earning more; it’s often about smart management of your deductions and effective financial planning. By strategically reviewing your withholdings and leveraging available benefits, you can effectively increase the amount of money you take home and improve your overall financial health.

A key strategy involves regularly reviewing your W-4 form to ensure your tax withholdings are accurate. Over-withholding means you’re giving the government an interest-free loan, while under-withholding can lead to a surprise tax bill. Finding the right balance is crucial for optimizing your cash flow throughout the year.

Reviewing W-4 Elections

Your W-4 form dictates how much federal income tax is withheld from each paycheck. Life changes such as marriage, having children, or taking on a second job should prompt a review of your W-4 to ensure your withholdings accurately reflect your current situation. This helps prevent large tax refunds or unexpected taxes due.

- Life Events: Adjust W-4 after marriage, birth of a child, or significant income changes.

- Tax Software: Utilize online calculators or tax software to estimate optimal withholdings.

- Annual Review: Make it a habit to check your W-4 at least once a year.

Taking full advantage of employer-sponsored benefits is another powerful way to optimize your financial health. Contributing to a 401(k) or 403(b), especially if there’s an employer match, is a no-brainer. These contributions reduce your taxable income and grow tax-deferred, significantly boosting your retirement savings.

Furthermore, consider flexible spending accounts (FSAs) or health savings accounts (HSAs) for healthcare or dependent care expenses. These accounts allow you to pay for qualified expenses with pre-tax dollars, effectively reducing your taxable income and increasing your net financial benefit. By being proactive and informed, you can make your paycheck work harder for you.

| Key Paycheck Component | Brief Description |

|---|---|

| Gross Pay | Total earnings before any deductions are applied. |

| Mandatory Deductions | Taxes required by law, such as federal, state, and FICA. |

| Voluntary Deductions | Optional withholdings for benefits like health insurance and retirement. |

| Net Pay | The actual amount received after all deductions are taken from gross pay. |

Frequently Asked Questions About Your 2026 Paycheck

Gross pay is your total earned income before any deductions. Net pay is the amount you actually receive after all mandatory and voluntary deductions, like taxes and benefits, have been subtracted from your gross pay. It’s your take-home amount.

The primary mandatory deductions include federal income tax, state income tax (if applicable in your state), and FICA taxes, which encompass Social Security and Medicare contributions. These are legally required withholdings for public services and social programs.

You can influence federal income tax withholding by adjusting your W-4 form. By claiming different allowances or specifying additional withholding amounts, you can fine-tune how much tax is taken out of each paycheck to better match your tax liability.

401(k) contributions are considered voluntary deductions. While highly recommended for retirement savings, you choose whether to contribute and how much. These contributions are typically pre-tax, which can reduce your current taxable income.

Understanding your paycheck deductions is crucial for accurate budgeting, financial planning, and ensuring your withholdings are correct. It helps you manage your cash flow, take advantage of benefits, and avoid tax surprises, empowering your overall financial health.

Conclusion

Ultimately, a thorough understanding of your paycheck in 2026, encompassing gross pay, mandatory and voluntary deductions, and the resulting net pay, is more than just an accounting exercise—it’s a critical component of personal financial education. By demystifying these elements, you gain greater control over your income, can make informed decisions about your benefits, and strategically plan for your financial future. Regularly reviewing your pay stub and staying informed about tax law changes will empower you to optimize your take-home pay and achieve your financial goals.