Digital Accounts vs. Traditional Banking: 2026 US Consumer Comparison

Anúncios

Understanding the evolving financial landscape in 2026, US consumers must critically evaluate the distinct benefits and drawbacks of digital accounts versus traditional banking, focusing on fees, features, and overall accessibility.

Anúncios

The financial world is always changing, and by 2026, US consumers have more choices than ever for managing their money. One of the biggest decisions involves choosing between digital accounts vs traditional banking. This comparison is not just about convenience; it’s about understanding fees, features, and how each option fits into your daily life.

Anúncios

The Evolution of Banking: Digital vs. Traditional Foundations

For decades, traditional banks were the only option, providing a sense of security and a physical presence. However, the rise of technology has brought about a new era of digital banking, challenging these long-held norms. Understanding the foundational differences between these two models is crucial for any US consumer navigating the 2026 financial landscape.

Traditional banks, often characterized by their brick-and-mortar branches, have a long history of providing comprehensive financial services. They offer a personal touch, allowing customers to interact directly with tellers and financial advisors. This model has been built on trust and a physical infrastructure that many still value.

Core Characteristics of Traditional Banking

- Physical Presence: Branches for in-person transactions and consultations.

- Established Trust: Decades or centuries of operation build consumer confidence.

- Comprehensive Services: Often a wider range of complex financial products.

Digital accounts, on the other hand, operate almost entirely online or through mobile apps, eliminating the need for physical branches. These institutions leverage technology to offer streamlined services, often at a lower cost. Their appeal lies in their accessibility and often user-friendly interfaces, designed for the modern, tech-savvy consumer.

Defining Digital Accounts

- Online-First Approach: All transactions and customer service are digital.

- Technological Innovation: Frequent updates and new features via apps.

- Accessibility: Manage finances anytime, anywhere with an internet connection.

The fundamental distinction lies in their operational models and how they interact with customers. Traditional banks prioritize a physical network and personal interactions, while digital accounts focus on efficiency, technology, and remote access. This divergence shapes everything from fee structures to the types of services offered, making a significant impact on consumer choice in 2026.

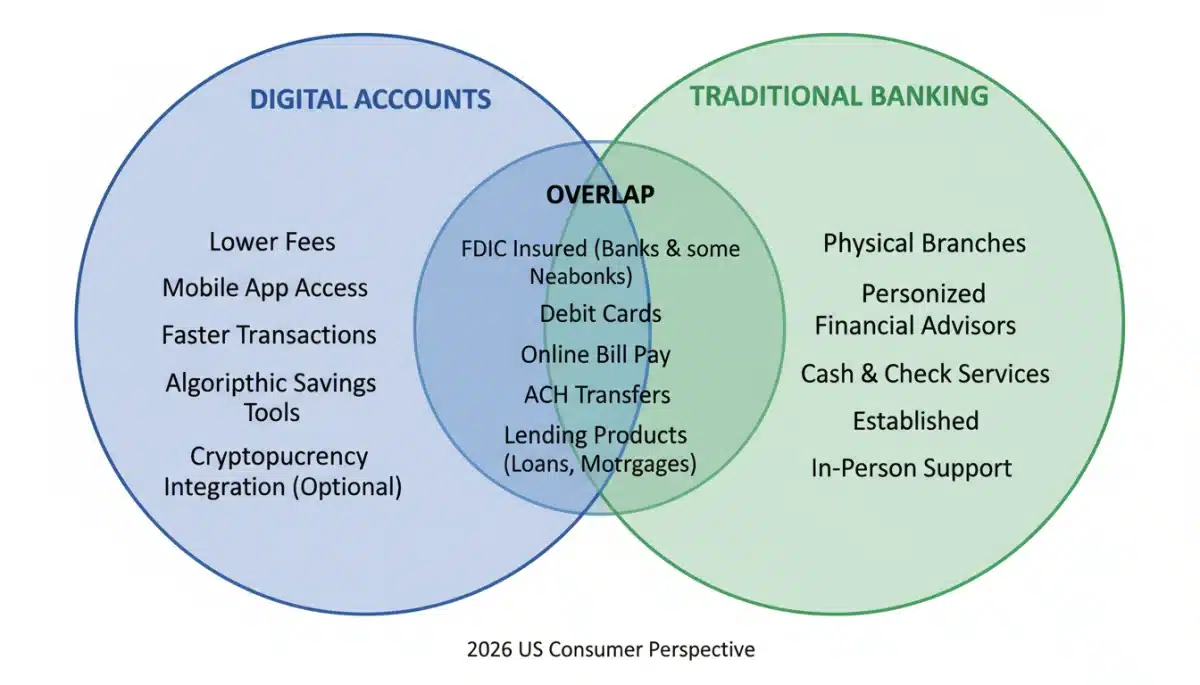

Fee Structures: A Closer Look at Costs in 2026

One of the most significant factors influencing the choice between digital accounts and traditional banking in 2026 is the fee structure. While both types of institutions charge fees, the nature and frequency of these charges can differ dramatically, directly impacting a consumer’s overall financial health.

Traditional banks often have a more extensive list of potential fees. These can include monthly maintenance fees, ATM fees (especially out-of-network), overdraft fees, wire transfer fees, and minimum balance fees. While many traditional banks offer ways to waive some of these fees, such as maintaining a certain balance or setting up direct deposit, they still represent a potential cost burden for many consumers.

Common Traditional Banking Fees

- Monthly Maintenance Fees: Often avoidable with specific account activity.

- ATM Fees: Can accrue rapidly if using non-bank ATMs.

- Overdraft Fees: Penalties for spending more than available funds.

- Wire Transfer Fees: Charges for sending money electronically to other banks.

Digital accounts, by contrast, are typically known for their lower or even nonexistent fees. Their reduced overhead costs, stemming from the lack of physical branches, allow them to pass these savings on to their customers. Many digital banks pride themselves on offering no monthly maintenance fees, free in-network ATM access, and transparent fee schedules.

Typical Digital Account Fee Advantages

- No Monthly Fees: A major draw for budget-conscious consumers.

- Lower ATM Fees: Often offer widespread fee-free ATM networks.

- Reduced Overdraft Penalties: Some offer grace periods or smaller fees.

However, it’s essential for consumers to read the fine print for both options. Some digital accounts might have less favorable foreign transaction fees or specific charges for certain services. Similarly, traditional banks are increasingly offering fee-free checking accounts to compete, though these often come with specific requirements. Ultimately, a careful comparison of fee schedules against personal banking habits is critical to determining the most cost-effective choice in 2026.

Feature Set Comparison: What Each Offers US Consumers

Beyond fees, the range of features and services offered by digital accounts and traditional banks plays a crucial role in decision-making for US consumers in 2026. Both types of institutions have evolved significantly, but their strengths and specialties remain distinct, catering to different financial needs and preferences.

Traditional banks often excel in offering a wide array of complex financial products and personalized services. This includes mortgages, auto loans, business banking services, investment advice, and wealth management. The ability to sit down with a financial advisor and discuss long-term financial planning is a significant advantage for many. They also typically provide services like safe deposit boxes and cashier’s checks, which digital-only banks may not offer.

Traditional Banking Feature Highlights

- Personalized Financial Advice: Access to dedicated advisors.

- Full-Service Lending: Mortgages, auto loans, and business financing.

- Specialized Services: Safe deposit boxes, notarization, and cashier’s checks.

Digital accounts, while typically more focused on everyday banking, shine in their technological innovation and convenience. They often boast highly intuitive mobile apps with advanced budgeting tools, instant transaction notifications, peer-to-peer payment integration, and early access to direct deposits. Many offer high-yield savings accounts, making it easier to grow savings without traditional bank overhead.

Digital Account Feature Strengths

- Advanced Mobile Apps: User-friendly interfaces with robust features.

- Budgeting Tools: Integrated analytics to track spending.

- Instant Payments: Seamless peer-to-peer transfers and bill pay.

- High-Yield Savings: Competitive interest rates on deposits.

The choice often boils down to a consumer’s priorities. If comprehensive financial planning, complex lending, and in-person support are paramount, traditional banking might be a better fit. If convenience, low fees, and cutting-edge digital tools for everyday money management are preferred, digital accounts present a compelling alternative. Many consumers in 2026 are also opting for a hybrid approach, leveraging the best of both worlds.

Security and Trust: Protecting Your Money in 2026

When it comes to managing money, security and trust are paramount, regardless of whether you choose a digital account or a traditional bank. In 2026, both financial models employ sophisticated measures to protect customer funds and data, though their approaches and perceived risks can differ.

Traditional banks benefit from a long-standing reputation and a physical presence, which often instills a sense of security. They are heavily regulated and subject to rigorous audits. Most importantly, deposits in traditional banks are typically FDIC-insured up to $250,000 per depositor, per insured bank, for each account ownership category. This federal insurance provides a critical safety net, assuring customers that their funds are protected even if the bank were to fail.

Traditional Banking Security Pillars

- FDIC Insurance: Federal protection for deposits.

- Physical Security: Branches offer a tangible layer of protection.

- Established Regulations: Strict adherence to financial laws.

Digital accounts operate without physical branches, leading some to question their security. However, the vast majority of reputable digital banks and fintech companies partner with FDIC-insured traditional banks to hold customer deposits, thereby extending the same federal protection. They also invest heavily in cybersecurity, employing advanced encryption, multi-factor authentication, and fraud detection systems to safeguard digital assets and personal information.

Digital Account Security Measures

- FDIC Pass-Through Insurance: Deposits are typically protected through partner banks.

- Advanced Cybersecurity: Encryption and fraud monitoring are standard.

- Multi-Factor Authentication: Extra layers of security for account access.

The perception of security can sometimes outweigh the reality. While a physical branch might feel more secure, cyber threats are a universal concern. Both traditional and digital institutions continuously update their security protocols to combat evolving threats. For US consumers in 2026, verifying FDIC insurance status for any financial institution, digital or traditional, is the most crucial step in ensuring the safety of their funds.

Accessibility and Convenience: Banking on Your Terms

Accessibility and convenience are key differentiators between digital accounts and traditional banking, profoundly impacting how US consumers manage their finances in 2026. The ideal choice often depends on an individual’s lifestyle, technological comfort, and specific banking needs.

Traditional banks offer unparalleled convenience for those who prefer or require in-person services. The ability to visit a branch for complex transactions, cash deposits, or face-to-face discussions with a banker remains a significant advantage for many. This physical accessibility is particularly important for cash-heavy businesses, older demographics, or those who simply prefer human interaction for sensitive financial matters. However, their accessibility is limited by branch hours and geographic location.

Traditional Banking Accessibility

- In-Person Services: Direct interaction with bank staff.

- Cash Handling: Easy cash deposits and withdrawals at branches.

- Local Presence: Community-oriented services and support.

Digital accounts redefine convenience by offering 24/7 access to banking services from virtually anywhere with an internet connection. Mobile apps allow users to check balances, pay bills, transfer funds, and even deposit checks remotely using their smartphone cameras. This constant accessibility is a major draw for busy individuals, frequent travelers, and those who prioritize speed and efficiency in their financial transactions.

Digital Account Convenience Factors

- 24/7 Access: Manage finances anytime, anywhere.

- Mobile-First Experience: Banking optimized for smartphones and tablets.

- Remote Deposits: Deposit checks via mobile app, eliminating branch visits.

While digital accounts excel in remote convenience, they can pose challenges for cash transactions, as they often rely on third-party ATMs or retail partnerships for deposits. Conversely, traditional banks, while offering physical access, might not provide the same level of digital innovation or always-on support. The best choice in 2026 hinges on a consumer’s preferred method of interaction and their need for either physical or digital convenience.

Emerging Trends and Future Outlook for Banking in 2026

The financial landscape is not static, and by 2026, both digital accounts and traditional banking are continuing to evolve, driven by technological advancements and changing consumer expectations. Understanding these emerging trends is crucial for US consumers looking to make informed decisions about their financial future.

Digital accounts are at the forefront of innovation, constantly integrating new technologies like artificial intelligence (AI) for personalized financial advice, machine learning for enhanced fraud detection, and open banking APIs for seamless integration with other financial apps. The trend towards hyper-personalization, where banking services are tailored to individual spending habits and financial goals, is rapidly gaining traction. We can expect even more sophisticated budgeting tools, predictive analytics, and automated savings features from digital providers.

Key Trends in Digital Banking

- AI-Powered Insights: Personalized financial guidance and recommendations.

- Open Banking Integration: Seamless connectivity with third-party financial tools.

- Hyper-Personalization: Tailored services based on individual financial behavior.

Traditional banks are not standing still. Many are investing heavily in their digital infrastructure, upgrading their mobile apps, offering more online services, and even experimenting with hybrid models that combine the best of both worlds. The focus for traditional institutions is often on leveraging their existing trust and comprehensive service offerings while adopting digital efficiencies. We’re seeing more traditional banks offer competitive digital-only products or enhanced online customer service to meet modern demands.

Traditional Banking’s Evolution

- Digital Transformation: Enhanced online platforms and mobile apps.

- Hybrid Models: Combining physical presence with digital convenience.

- Focus on Customer Experience: Integrating technology to improve service.

The future of banking in 2026 likely points towards a convergence, where the lines between traditional and digital become increasingly blurred. Consumers will benefit from more choices, with institutions offering a blend of robust digital features and personalized support. The key for US consumers will be to remain adaptable and informed about these evolving options to secure the best financial services for their needs.

Making the Right Choice: A 2026 Consumer Guide

Deciding between digital accounts and traditional banking in 2026 is a personal choice that hinges on individual financial habits, priorities, and comfort levels with technology. There’s no one-size-fits-all answer; instead, it requires a thoughtful assessment of what truly matters for your money management.

Consider your banking frequency and preferred interaction methods. If you rarely visit a physical branch, prefer to manage everything from your smartphone, and prioritize low fees and innovative digital tools, a digital account might be the ideal solution. These accounts are often best for those comfortable with technology and who value efficiency and accessibility above all else.

Who Benefits Most from Digital Accounts?

- Tech-Savvy Individuals: Those comfortable with mobile apps and online platforms.

- Budget-Conscious Consumers: Individuals prioritizing low or no fees.

- Frequent Travelers: People needing constant access to their finances on the go.

Conversely, if you value in-person consultations, frequently handle cash, require complex lending products like mortgages, or simply prefer the tangible security of a physical bank, a traditional institution may be a better fit. These banks provide a human touch and a broader range of specialized services that digital-only platforms may not fully replicate.

Who Benefits Most from Traditional Banking?

- Individuals Needing Personal Advice: Those seeking face-to-face financial planning.

- Cash-Heavy Users: Consumers who frequently deposit or withdraw physical cash.

- Complex Financial Needs: Individuals requiring mortgages, business loans, or wealth management.

Many US consumers in 2026 are finding a hybrid approach to be the most effective strategy. This involves using a digital account for everyday spending and savings due to its convenience and low fees, while maintaining a traditional bank account for specific needs like large loans, complex transactions, or the occasional need for in-person support. Ultimately, the right choice is the one that aligns best with your financial lifestyle and provides the peace of mind and functionality you need.

| Key Aspect | Comparison Summary |

|---|---|

| Fees | Digital accounts often have lower or no monthly fees; traditional banks may have more fees, often waivable with conditions. |

| Features | Digital excels in mobile apps, budgeting tools, and high-yield savings; traditional offers comprehensive lending and in-person advice. |

| Accessibility | Digital provides 24/7 online access; traditional offers physical branches for in-person transactions and cash handling. |

| Security | Both are generally FDIC-insured (digital often via partners) and employ robust cybersecurity measures. |

Frequently Asked Questions About Banking in 2026

Yes, most reputable digital accounts in 2026 are FDIC-insured, typically through partnerships with traditional banks. This means your deposits are protected up to $250,000, just like with a traditional bank. Always verify the FDIC status of any financial institution you choose.

Depositing cash into a digital account can be done through various methods in 2026, including retail partnerships (like at major drugstores), money orders, or by transferring funds from a traditional bank account. Direct cash deposits at a digital bank’s ‘branch’ are usually not an option.

Generally, digital accounts tend to have lower fees, often boasting no monthly maintenance fees and reduced ATM charges. Traditional banks may have more fees, but many offer ways to waive them if certain conditions, like direct deposit or minimum balances, are met.

Absolutely. In 2026, traditional banks are heavily investing in digital transformation, enhancing their mobile apps, improving online services, and integrating modern features to compete with purely digital offerings. Many are moving towards hybrid models to serve a broader customer base.

Yes, a hybrid approach is increasingly popular in 2026. Many US consumers use digital accounts for everyday banking and savings due to their convenience and low costs, while maintaining a traditional bank account for specific needs like large loans, complex transactions, or in-person support.

Conclusion

The choice between digital accounts and traditional banking in 2026 for US consumers is more nuanced than ever. Each option presents a unique set of advantages and disadvantages concerning fees, features, security, and accessibility. Digital accounts offer unparalleled convenience and often lower costs, ideal for the tech-savvy individual. Traditional banks provide a sense of established trust, comprehensive services, and a physical presence for those who value personal interaction and specialized lending. As the financial landscape continues to evolve, understanding your personal financial needs and preferences will be the ultimate guide in selecting the banking solution that best empowers your financial well-being.