Hidden Fees in Digital Accounts: 2026 Insider Guide

Anúncios

Understanding and proactively managing potential charges is crucial for consumers to avoid unexpected costs and maintain financial health in the evolving digital account landscape of 2026.

Anúncios

Are you truly in control of your digital finances? In 2026, navigating the world of digital accounts can feel like a minefield, with potential digital account hidden fees lurking around every corner. This guide provides insider knowledge to help you identify and avoid those unnecessary charges, ensuring your money stays where it belongs: in your pocket.

Anúncios

The evolving landscape of digital account fees in 2026

The financial world has undergone a rapid transformation, with digital accounts becoming the norm for millions of Americans. While these accounts offer unparalleled convenience, they also introduce a new set of complexities, particularly regarding fees. What might have been a straightforward transaction a few years ago could now carry a subtle, often overlooked charge.

Understanding this evolving landscape is the first step toward financial vigilance. Banks and fintech companies are constantly innovating, and with that innovation comes new revenue streams, sometimes at the consumer’s expense. Staying informed about these changes is not just advisable; it’s essential.

Why fees are more prevalent in digital accounts

Digital platforms often operate with lower overheads than traditional brick-and-mortar banks, leading many to assume they are fee-free. However, this isn’t always the case. The shift to digital has opened doors for new types of charges, often tied to specific services or usage patterns. These can range from micro-transaction fees to charges for premium features that might seem negligible individually but add up significantly over time.

- Lower operational costs for providers do not always translate to zero fees for users.

- New digital services often come with their own fee structures.

- The competitive nature of the digital banking market can sometimes lead to opaque fee disclosures as providers vie for market share.

The challenge of transparency in a digital-first world

Despite regulations aimed at transparency, the sheer volume of digital financial products and the speed at which they evolve can make it challenging for consumers to keep track. Disclosures are often buried in lengthy terms and conditions documents or presented in a way that requires careful scrutiny. This makes it difficult for the average user to fully grasp the potential costs associated with their digital accounts.

The goal of this section is to set the stage, emphasizing that while digital accounts are convenient, they demand a proactive approach to fee management. The financial ecosystem of 2026 requires a keen eye and a commitment to understanding the fine print.

Identifying common hidden fees in your digital accounts

Many digital account users are unaware of the various charges that can silently erode their balances. These aren’t always the obvious monthly maintenance fees; often, they are subtle, transactional charges that accumulate over time. Knowing what to look for is half the battle.

Identifying these hidden fees requires a careful review of your account statements and an understanding of how your digital account provider operates. It’s about looking beyond the headline promises of ‘free’ banking and delving into the specifics of their fee schedule.

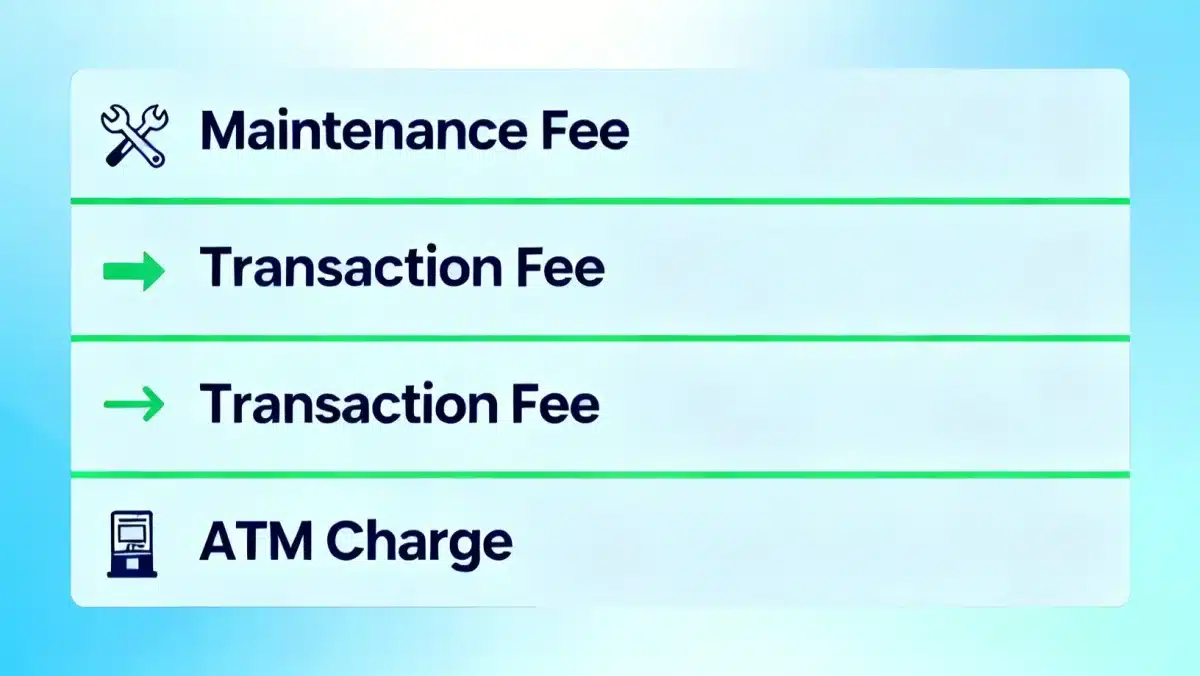

Transaction-based charges you might overlook

One of the most common categories of hidden fees revolves around transactions. These can include charges for certain types of transfers, foreign transaction fees, or even fees for using specific payment networks. While individual charges might be small, frequent use can lead to substantial costs.

- ATM withdrawal fees: Even if your bank doesn’t charge, the ATM owner might.

- Foreign transaction fees: Using your digital card abroad often incurs a percentage-based fee.

- Expedited transfer fees: Paying extra to send money faster can add up.

Maintenance and inactivity fees: the silent drain

Some digital accounts, despite being marketed as low-cost, may still impose maintenance fees under certain conditions, such as not meeting a minimum balance or failing to make a certain number of transactions per month. Inactivity fees are another common culprit, penalizing users for not using their account often enough.

These fees are particularly insidious because they often go unnoticed until a significant amount has been deducted. Regularly checking your account’s terms and conditions, especially any updates, is crucial to avoid these unexpected deductions. This section aims to equip you with the knowledge to spot these common but often hidden charges, enabling you to take proactive measures.

Strategies for avoiding unnecessary digital account charges

Once you’ve identified the types of hidden fees that can affect your digital accounts, the next step is to implement strategies to avoid them. This isn’t just about being aware; it’s about actively managing your account usage and making informed choices about your financial providers.

Avoiding these charges often involves a combination of careful planning, understanding your account’s specific rules, and sometimes, even switching providers if the fees become too burdensome. The goal is to minimize your outgoing expenses and maximize your savings.

Choosing the right digital account provider

Not all digital accounts are created equal. Some providers genuinely offer robust services with minimal fees, while others have more complex fee structures. Thoroughly researching and comparing different options before committing is vital. Look for providers that align with your typical usage patterns and offer transparent fee schedules.

- Compare monthly fees, transaction costs, and ATM policies.

- Read reviews and look for common complaints about hidden charges.

- Prioritize providers with clear and easily accessible fee disclosures.

Leveraging fee-free features and services

Many digital accounts come with a range of fee-free features that users might not fully utilize. This could include free ATM networks, free peer-to-peer transfers, or no-fee international transactions up to a certain limit. By understanding and actively using these features, you can significantly reduce your overall costs.

For instance, if your digital bank offers a specific ATM network that provides fee-free withdrawals, make it a point to use those ATMs. Similarly, if there’s a limit on fee-free international transfers, plan your overseas transactions accordingly. This proactive approach can lead to considerable savings over time.

The impact of fintech innovations on digital account fees

Fintech, or financial technology, is continually reshaping the banking industry. While many innovations aim to make financial services more accessible and affordable, they can also introduce new fee models that users need to be aware of. The rapid pace of change means that what was true about fees last year might not be true today.

Understanding the interplay between fintech innovations and fee structures is crucial for staying ahead. New services, while convenient, often come with their own pricing, and it’s up to the consumer to evaluate whether the benefits outweigh the costs.

Subscription models and premium features

A growing trend in fintech is the move towards subscription-based models for premium digital account features. While basic accounts might be free, enhanced services like advanced budgeting tools, higher interest rates on savings, or dedicated customer support often come with a monthly fee. These are not always ‘hidden’ but can be easily overlooked if consumers don’t fully understand what their subscription entails.

Before opting for any premium features, assess whether the added benefits genuinely justify the recurring cost. Sometimes, the free tier of a digital account is sufficient for most users, and paying for premium services might be an unnecessary expense.

Micro-fees and bundled services

Fintech companies sometimes employ micro-fees for specific, small-value transactions or services. These fees, while individually tiny, can accumulate rapidly, especially for active users. Another strategy is bundling services, where a single fee covers multiple offerings. While this can seem convenient, it’s important to ensure you’re actually using all the bundled services to justify the cost.

- Be wary of small, frequent charges that appear on your statement.

- Evaluate bundled services to ensure you’re getting value for money.

- Regularly review your usage patterns against your account’s fee structure.

By staying informed about these fintech trends, you can make more strategic decisions about which digital accounts and services best suit your financial needs without incurring unexpected charges.

Leveraging technology to monitor and manage fees

In 2026, technology isn’t just the source of some fees; it’s also your most powerful ally in managing and avoiding them. A variety of digital tools and services are available to help you monitor your accounts, track your spending, and identify any unusual or unexpected charges.

Embracing these technological solutions can transform a passive approach to financial management into an active, informed one. These tools provide real-time insights, alerts, and detailed breakdowns of your financial activity, making it much harder for hidden fees to slip through the cracks.

Budgeting apps and financial aggregators

Modern budgeting apps and financial aggregators can connect to all your digital accounts, providing a holistic view of your finances. Many of these tools offer features that categorize spending, track subscriptions, and even flag unusual transactions, which can include hidden fees. By regularly reviewing these aggregated insights, you can quickly spot discrepancies.

- Use apps that offer detailed transaction categorization.

- Set up alerts for transactions above a certain amount or from unfamiliar sources.

- Regularly check your spending reports for recurring small charges you don’t recognize.

AI-powered fee detection and negotiation tools

The rise of artificial intelligence has introduced sophisticated tools capable of analyzing your financial statements for potential fees that could be waived or negotiated. Some AI-powered services can even identify if you’re paying more than necessary for certain services and suggest alternatives or help you negotiate with your providers.

While these tools are still evolving, they represent a significant step forward in consumer empowerment. They can act as your personal financial assistant, tirelessly working to optimize your spending and identify areas where you might be overpaying. Exploring these advanced solutions can be a game-changer in your fight against hidden fees.

Advocacy and consumer rights in digital banking

Even with the best strategies, hidden fees can sometimes appear. When they do, knowing your rights as a consumer and how to advocate for yourself is paramount. The regulatory landscape is constantly adapting to the digital age, offering avenues for consumers to dispute unfair charges.

Being an informed and assertive consumer can make a significant difference. Don’t assume that a fee is non-negotiable or that you have no recourse. Many digital banks value their customer relationships and are willing to resolve legitimate concerns.

Understanding regulatory protections for digital accounts

In the United States, several federal agencies oversee financial institutions, including those offering digital accounts. The Consumer Financial Protection Bureau (CFPB) is a key player, working to ensure transparency and fairness in financial products and services. Familiarizing yourself with the protections offered by these bodies can empower you to challenge unfair fees.

These protections often cover requirements for clear disclosure of fees, limits on certain types of charges (like overdraft fees), and procedures for resolving disputes. Knowing these rights is your first line of defense against exploitative practices.

Steps to dispute an unfair digital account fee

If you encounter a fee you believe is unfair or incorrectly applied, don’t hesitate to take action. The process usually begins by contacting your digital account provider directly. Document all communications, including dates, times, and the names of representatives you speak with.

- Review your account terms and conditions to confirm the fee’s legitimacy.

- Contact customer support, clearly stating your case and providing any relevant evidence.

- If unsatisfied, escalate your complaint to a supervisor or through the company’s official complaint channels.

- Consider filing a complaint with the CFPB or other relevant regulatory bodies if the issue remains unresolved.

Being persistent and methodical in your dispute can often lead to a favorable outcome, whether it’s a fee waiver or a clear explanation of the charge. This section underscores the importance of consumer vigilance and the power of informed advocacy.

Future trends in digital account fees: what to expect by 2026 and beyond

The financial world is dynamic, and understanding future trends in digital account fees is essential for long-term financial planning. By 2026, we can expect further innovations and regulatory changes that will continue to shape how fees are structured and disclosed.

Staying ahead of these trends means being prepared for potential shifts in fee models, new types of charges, and evolving consumer protections. This forward-looking perspective helps you adapt your strategies to maintain financial efficiency.

Personalization and dynamic pricing models

As AI and data analytics become more sophisticated, digital account providers may increasingly move towards personalized and dynamic pricing. This could mean that fees are tailored to individual user behavior, credit scores, or even real-time market conditions. While this could offer benefits for some, it also introduces complexity in comparing services.

Consumers will need to be more diligent than ever in understanding their personalized fee structures and how their actions might influence them. The ‘one size fits all’ fee schedule may become a relic of the past for many digital financial products.

Increased regulatory scrutiny and consumer demand for transparency

As hidden fees become a more prominent issue, it’s likely that regulatory bodies will increase their scrutiny of digital account providers. Consumer groups are also advocating for greater transparency and simpler fee structures. This pressure could lead to new regulations requiring clearer disclosures and limiting certain types of charges.

While regulatory changes can be slow, the trend towards greater consumer protection is strong. Staying informed about these developments can help you anticipate how your digital accounts might be affected and when new opportunities for fee avoidance might arise. This section provides a glimpse into the future, encouraging continuous learning and adaptation.

| Key Point | Brief Description |

|---|---|

| Evolving Fee Landscape | Digital accounts introduce new fee complexities, requiring constant vigilance from users. |

| Common Hidden Fees | Look out for transaction, maintenance, and inactivity charges that often go unnoticed. |

| Proactive Avoidance | Choose suitable providers, leverage fee-free features, and monitor account terms regularly. |

| Future Trends & Advocacy | Anticipate personalized fees, increased regulation, and know your rights for dispute resolution. |

Frequently asked questions about digital account fees

The most common hidden fees include ATM withdrawal fees outside network, foreign transaction fees, expedited transfer charges, and sometimes maintenance or inactivity fees. These often appear as small, frequent deductions that can accumulate significantly over time if not monitored closely.

Regularly review your detailed transaction history. Look for small, unfamiliar charges, especially those labeled as ‘service fees’, ‘network fees’, or ‘transaction charges’. Compare your statement against your account’s official fee schedule to spot discrepancies or unexpected deductions.

While completely avoiding all fees might be challenging, it’s certainly possible to minimize them significantly. Choosing digital accounts with transparent, low-fee structures, utilizing fee-free features, and actively managing your account usage according to its terms can help reduce costs dramatically.

Fintech innovations introduce new fee models like subscription services for premium features and micro-fees for specific transactions. While offering convenience, these require users to carefully evaluate if the benefits outweigh the costs and to be aware of how their usage impacts these new charges.

First, contact your digital account provider’s customer support with documentation. If unresolved, escalate your complaint internally. If still not satisfied, consider filing a formal complaint with consumer protection agencies like the Consumer Financial Protection Bureau (CFPB) for assistance.

Conclusion

Navigating the complex world of digital account fees in 2026 demands vigilance and informed action. By understanding the evolving fee landscape, identifying common hidden charges, and implementing proactive avoidance strategies, you can protect your finances. Leveraging technology for monitoring and knowing your consumer rights are crucial steps. As the financial sector continues to innovate, staying informed about future trends will empower you to maintain control over your digital accounts, ensuring you only pay for the services you truly value.