Insurance Basics 2026: Protect Your Assets

Anúncios

Understanding insurance in 2026 is fundamental for financial education, offering robust protection for your assets against unforeseen risks and ensuring long-term financial stability.

Anúncios

In an increasingly complex world, grasping the basics of insurance in 2026: a financial education guide to protecting your assets is not just advisable, it’s essential. Are you prepared for the unexpected? This guide will illuminate how insurance acts as your financial fortress, helping you navigate potential pitfalls and secure your future.

Anúncios

Understanding the Core Purpose of Insurance in 2026

Insurance, at its heart, is a contract designed to protect you from financial loss. In exchange for regular payments, known as premiums, an insurance company promises to compensate you or your beneficiaries in the event of a specified loss. This fundamental principle remains unchanged in 2026, though the types of risks and available coverages continue to evolve with societal and technological advancements.

The primary goal is risk mitigation. Instead of bearing the full burden of an unexpected event, you transfer a portion of that risk to an insurer. This collective pooling of risk allows individuals to protect themselves from potentially catastrophic financial setbacks, making the unpredictable more manageable.

The Evolution of Risk and Coverage

The landscape of risk is constantly shifting. Cybersecurity threats, climate-related events, and even new health concerns influence the types of insurance products available. Understanding these evolving risks is crucial for selecting appropriate coverage. Insurers are now offering more specialized policies to address these modern challenges, emphasizing the need for ongoing financial education.

- Cyber Insurance: Protecting against data breaches and online fraud.

- Parametric Insurance: Triggered by specific events like earthquake intensity, rather than actual damage assessment.

- Digital Asset Protection: Coverage for cryptocurrencies and NFTs, reflecting new economic realities.

Ultimately, the purpose of insurance is to provide peace of mind. Knowing that you have a safety net in place allows you to pursue opportunities and live your life with greater confidence, minimizing the fear of financial ruin from unforeseen circumstances. It’s an investment in your stability.

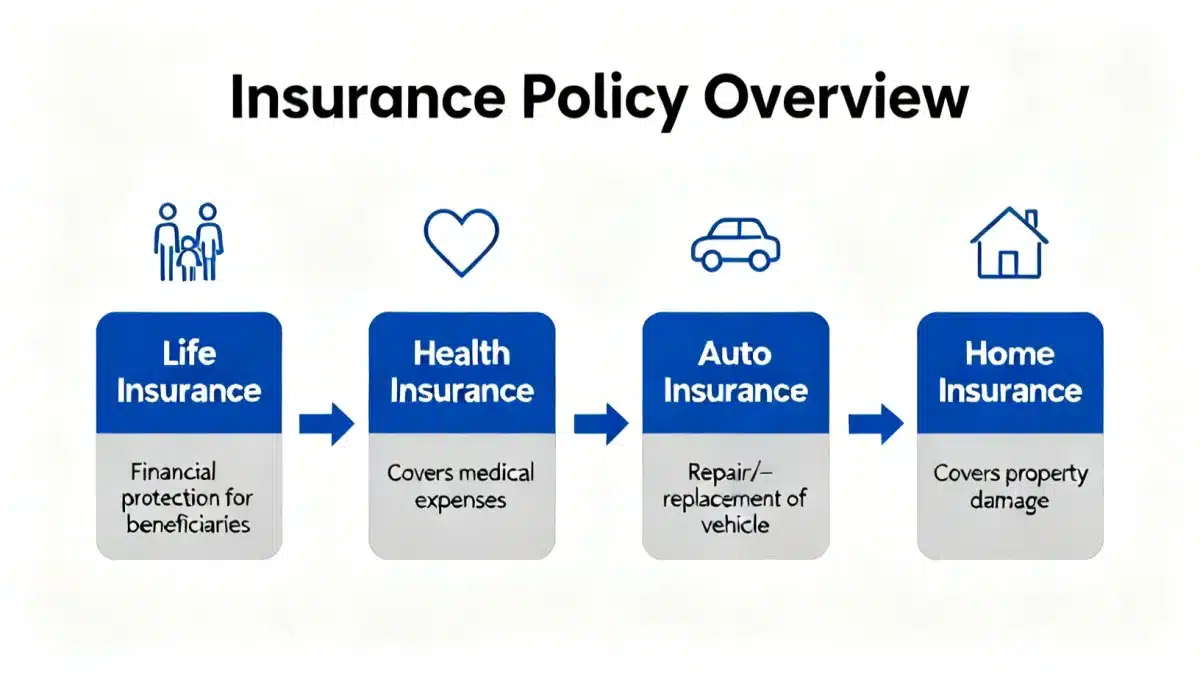

Key Types of Insurance for Personal Asset Protection

Protecting your assets in 2026 requires a comprehensive understanding of the various insurance types available. Each category serves a distinct purpose, safeguarding different aspects of your life and finances. From your home to your health, strategic insurance choices form the bedrock of a robust financial plan.

Navigating the array of options can seem daunting, but breaking them down into core categories simplifies the process. It’s about identifying your personal vulnerabilities and matching them with the right protective measures.

Health Insurance: Your Wellness Shield

Health insurance is paramount, covering medical expenses, prescription drugs, and sometimes even preventative care. In the United States, options typically include employer-sponsored plans, marketplace plans under the Affordable Care Act (ACA), and government programs like Medicare and Medicaid. Choosing the right plan involves weighing premiums, deductibles, co-pays, and out-of-pocket maximums against your anticipated healthcare needs.

- PPO (Preferred Provider Organization): More flexibility in choosing doctors and hospitals.

- HMO (Health Maintenance Organization): Requires choosing a primary care provider and referrals for specialists.

- HDHP (High-Deductible Health Plan): Often paired with a Health Savings Account (HSA) for tax-advantaged savings.

Auto Insurance: On the Road Protection

Legally mandated in most states, auto insurance protects against financial losses from accidents and theft. Beyond liability coverage, which pays for damages and injuries you cause to others, comprehensive and collision coverages are crucial for protecting your own vehicle. Uninsured/underinsured motorist coverage is also vital, especially in areas with high rates of uninsured drivers.

Homeowner’s/Renter’s Insurance: Securing Your Dwelling

Homeowner’s insurance protects your property and belongings from perils like fire, theft, and natural disasters, while also providing liability coverage. Renter’s insurance, often overlooked, is equally important for those who don’t own their home, covering personal possessions and liability within a rented space. Both are critical for preventing significant financial strain from property damage or legal claims.

Selecting the right personal asset protection involves a careful assessment of your individual circumstances, risk tolerance, and financial capacity. It’s not a one-size-fits-all solution; rather, it’s a tailored approach to building a resilient financial future.

Life Insurance: A Legacy of Security for Your Loved Ones

Life insurance stands as a cornerstone of long-term financial planning, offering a critical safety net for your family and dependents should you pass away. It’s not about your life, but about the financial well-being of those you leave behind, ensuring they can maintain their standard of living, cover debts, and achieve future goals.

The decision to purchase life insurance is deeply personal, driven by a desire to provide security and peace of mind for your loved ones. It reflects a commitment to their future, even in your absence.

Term Life Insurance: Simplicity and Affordability

Term life insurance provides coverage for a specific period, typically 10, 20, or 30 years. It’s often the most straightforward and affordable option, making it ideal for individuals seeking coverage during their prime earning years or until specific financial obligations, like a mortgage, are met. If you pass away within the term, your beneficiaries receive a tax-free death benefit.

- Level Term: Premiums and death benefit remain constant throughout the term.

- Decreasing Term: Death benefit decreases over the term, often used to cover a decreasing debt like a mortgage.

- Convertible Term: Allows conversion to a permanent policy without new medical exams.

Whole Life Insurance: Lifetime Coverage and Cash Value

Unlike term life, whole life insurance offers coverage for your entire life, provided premiums are paid. A significant feature of whole life policies is their cash value component, which grows tax-deferred over time. This cash value can be borrowed against or withdrawn, offering a potential source of funds later in life. While more expensive than term life, it provides lifelong protection and a savings element.

Universal Life Insurance: Flexibility and Customization

Universal life insurance offers more flexibility than whole life. Policyholders can often adjust premium payments and death benefits within certain limits, making it adaptable to changing financial circumstances. Like whole life, it also includes a cash value component that grows over time. This flexibility can be appealing for those whose financial needs may evolve significantly.

Choosing the right life insurance policy requires careful consideration of your family’s current and future financial needs, your budget, and your long-term financial goals. It’s a crucial step in building a resilient financial legacy.

Understanding Premiums, Deductibles, and Coverage Limits

Delving into the mechanics of insurance policies means understanding key terms like premiums, deductibles, and coverage limits. These elements directly impact both the cost of your insurance and the extent of protection you receive. A clear grasp of these concepts is vital for making informed decisions and optimizing your insurance strategy in 2026.

These terms are interconnected; adjusting one often affects the others. Finding the right balance allows you to manage costs while ensuring adequate protection.

Premiums: The Cost of Protection

A premium is the amount you pay, typically monthly, quarterly, or annually, to keep your insurance policy active. Factors influencing premiums include your age, health, location, claims history, and the type and amount of coverage you select. For instance, a younger, healthier individual will generally pay lower life insurance premiums than an older person with pre-existing conditions.

In auto insurance, your driving record and the type of vehicle you drive significantly impact your premium. Similarly, for home insurance, the age and construction of your home, as well as its location, play a role. Shopping around and comparing quotes from different providers can help you find competitive rates without sacrificing essential coverage.

Deductibles: Your Share of the Loss

A deductible is the amount of money you must pay out-of-pocket before your insurance coverage kicks in. For example, if you have a $1,000 deductible on your auto insurance and incur $3,000 in damages, you’ll pay the first $1,000, and your insurer will cover the remaining $2,000. Higher deductibles typically result in lower premiums, as you’re taking on more of the initial risk.

This trade-off requires careful consideration. While a high deductible can save you money on premiums, it also means you’ll need to have sufficient funds readily available to cover that initial cost in an emergency. It’s a strategic decision balancing immediate savings against potential future expenses.

Coverage Limits: The Maximum Payout

Coverage limits represent the maximum amount an insurance company will pay out for a covered loss. For example, your auto insurance might have a $100,000 liability limit per person, meaning the insurer will pay up to that amount for injuries you cause to one individual in an accident. Exceeding this limit would leave you personally responsible for the difference.

It’s crucial to ensure your coverage limits are adequate for your assets and potential liabilities. Underinsuring could lead to significant financial exposure in the event of a major claim. Regularly reviewing your policies and adjusting limits as your assets or circumstances change is a vital part of proactive financial management.

Mastering these terms empowers you to tailor your insurance policies effectively, ensuring you have the right level of protection at a cost that aligns with your financial plan.

The Role of Insurance in Comprehensive Financial Planning

Integrating insurance into your overall financial plan is not merely an afterthought; it’s a foundational component. In 2026, a holistic approach to financial education emphasizes that insurance acts as a protective layer, safeguarding all other aspects of your financial strategy, from investments to retirement savings. Without proper coverage, a single unforeseen event could derail years of careful planning.

Consider insurance as the risk management arm of your financial portfolio. It provides a buffer, allowing your investments to grow without the constant threat of being liquidated to cover emergencies.

Protecting Your Investments and Savings

Imagine building a substantial investment portfolio or diligently saving for retirement. Without adequate health insurance, a major medical emergency could deplete those funds. Similarly, lacking homeowner’s insurance could force you to use savings to rebuild after a disaster. Insurance preserves your capital by absorbing the financial shock of such events, allowing your other assets to remain intact and grow.

Debt Protection and Legacy Planning

Life insurance, in particular, plays a critical role in debt protection. It ensures that your family isn’t burdened with outstanding mortgages, loans, or other debts should you pass away. Beyond debt, it’s a powerful tool for legacy planning, enabling you to leave an inheritance, fund a child’s education, or support charitable causes, all while providing your beneficiaries with financial stability.

- Estate Planning: Life insurance can help cover estate taxes and ensure smooth asset transfer.

- Business Continuity: Key person insurance protects businesses from the financial loss due to the death or disability of a crucial employee.

- Long-Term Care Planning: Long-term care insurance can protect retirement savings from the high costs of extended care.

Effective financial planning in 2026 demands a proactive stance on risk. By strategically incorporating various types of insurance, you not only protect your current assets but also fortify your future financial goals against life’s inevitable uncertainties. It’s about building resilience into your wealth management strategy.

Emerging Trends and Future of Insurance in 2026

The insurance industry is not static; it’s constantly evolving, driven by technological advancements, changing consumer expectations, and new types of risks. In 2026, several key trends are shaping the future of insurance, offering both challenges and opportunities for policyholders. Staying informed about these developments is a crucial aspect of modern financial education.

From AI-powered underwriting to personalized policies, the future promises more tailored and efficient insurance solutions.

AI and Machine Learning in Underwriting

Artificial intelligence and machine learning are revolutionizing how insurers assess risk and determine premiums. By analyzing vast amounts of data, AI can identify patterns and predict risks with greater accuracy than traditional methods. This leads to more personalized policies and potentially fairer pricing based on individual risk profiles.

- Personalized Premiums: Rates adjusted based on real-time data from wearables (health) or telematics (auto).

- Faster Claims Processing: AI-driven tools streamline claims assessment and payout, reducing wait times.

- Fraud Detection: Advanced algorithms help identify and prevent fraudulent claims more effectively.

Parametric Insurance and Climate Change

With the increasing frequency and intensity of climate-related events, parametric insurance is gaining prominence. Instead of assessing actual damage, these policies pay out a pre-agreed amount when a specific parameter is met (e.g., hurricane wind speed, earthquake magnitude). This offers quicker payouts and reduces disputes, providing a more immediate financial lifeline after a disaster.

Embedded Insurance and Digital Integration

Embedded insurance, where coverage is seamlessly integrated into the purchase of a product or service, is becoming more common. For example, buying travel insurance directly when booking a flight, or product protection plans offered at the point of sale. This trend makes insurance more accessible and convenient, often without the consumer having to seek it out separately.

The future of insurance in 2026 is characterized by greater personalization, efficiency, and responsiveness to emerging global challenges. As a policyholder, understanding these trends can help you leverage new products and technologies to optimize your protection and financial security.

Choosing the Right Insurance Provider and Policy

Selecting the appropriate insurance provider and policy is a critical decision that can significantly impact your financial well-being. It goes beyond just comparing prices; it involves evaluating the insurer’s reputation, financial stability, customer service, and the fine print of the policy itself. Making an informed choice ensures you receive reliable protection when you need it most.

The cheapest option isn’t always the best. Value often lies in a combination of comprehensive coverage, excellent service, and a trustworthy provider.

Researching Insurer Reputation and Financial Strength

Before committing to a policy, thoroughly research the insurance company. Look for reviews from current and former policyholders regarding their claims process and customer support. Financial strength ratings from independent agencies like A.M. Best, Standard & Poor’s, or Moody’s provide insights into an insurer’s ability to pay out claims, which is paramount in times of crisis.

Comparing Policy Details and Understanding the Fine Print

Don’t just look at the premium. Dive deep into the policy’s terms and conditions. Understand what is covered, what is excluded, and any specific conditions that must be met for a claim to be valid. Pay attention to deductibles, coverage limits, and any riders or endorsements that might be necessary to tailor the policy to your specific needs. Ask questions if anything is unclear.

- Read the Policy Document: The full contract contains all the details.

- Check for Exclusions: What specific events or conditions are NOT covered?

- Understand Claim Procedures: What steps are required to file a claim?

Leveraging Independent Agents and Online Tools

Independent insurance agents can be invaluable resources. They work with multiple insurance companies and can help you compare various policies and providers, often finding options that best suit your needs and budget. Additionally, numerous online comparison tools allow you to get quotes from multiple insurers simultaneously, streamlining the shopping process.

Ultimately, choosing the right insurance provider and policy is about finding a balance between cost, coverage, and trust. A well-chosen policy provides peace of mind, knowing that your assets are protected by a reliable partner.

| Key Point | Brief Description |

|---|---|

| Risk Mitigation | Insurance transfers financial risk from individuals to an insurer, protecting against unforeseen losses. |

| Asset Protection | Various policies (health, auto, home, life) protect different assets and provide financial security. |

| Core Terms | Understand premiums (cost), deductibles (out-of-pocket), and coverage limits (max payout). |

| Future Trends | AI, parametric insurance, and embedded policies are shaping the evolving insurance landscape. |

Frequently Asked Questions About Insurance in 2026

In 2026, increased financial complexities, evolving digital risks, and climate-related uncertainties make insurance crucial. It provides a vital safety net against these modern challenges, protecting assets and ensuring financial stability in an unpredictable world. It’s an indispensable component of sound financial planning.

Determining adequate coverage involves assessing your assets, liabilities, and potential risks. For life insurance, consider your family’s financial needs. For property, ensure coverage matches replacement costs. Consulting with a financial advisor can help tailor coverage to your specific situation, balancing protection with affordability.

A high deductible typically leads to lower monthly insurance premiums, saving you money on recurring costs. This can be beneficial if you have sufficient emergency savings to cover the initial out-of-pocket expense in case of a claim. It’s a strategic choice for managing immediate budget concerns while maintaining coverage.

Yes, in 2026, specialized insurance products are emerging to cover digital assets such as cryptocurrency and NFTs. These policies often protect against theft, cyberattacks, and certain types of fraud. As the digital economy grows, insurers are adapting to provide necessary protection for these new forms of wealth.

It’s advisable to review your insurance policies at least annually, or whenever a significant life event occurs. This includes marriage, birth of a child, purchasing a new home or car, or a major change in income. Regular reviews ensure your coverage remains adequate and aligned with your current needs.

Conclusion

Navigating the basics of insurance in 2026: a financial education guide to protecting your assets is an indispensable part of securing your financial future. As the economic and risk landscapes continue to evolve, a clear understanding of various insurance types, their mechanics, and their role in comprehensive financial planning is more critical than ever. By making informed choices about premiums, deductibles, and coverage limits, and by staying abreast of emerging industry trends, individuals can effectively safeguard their assets, protect their loved ones, and build a resilient foundation for long-term financial stability. Insurance isn’t just a safety net; it’s a strategic tool for peace of mind and sustained prosperity.